How to address concentration risk in portfolio construction? Today we will explore different ways to design an index that tilts so heavily to the largest constituents while keeping an eye on tradability and risk management.

Historically, index providers have used fixed weight capping to mitigate large concentration in one or more securities, where the extra weight is redistributed to smaller non capped constituents. Recall from our first blog in the series the weights as follows:

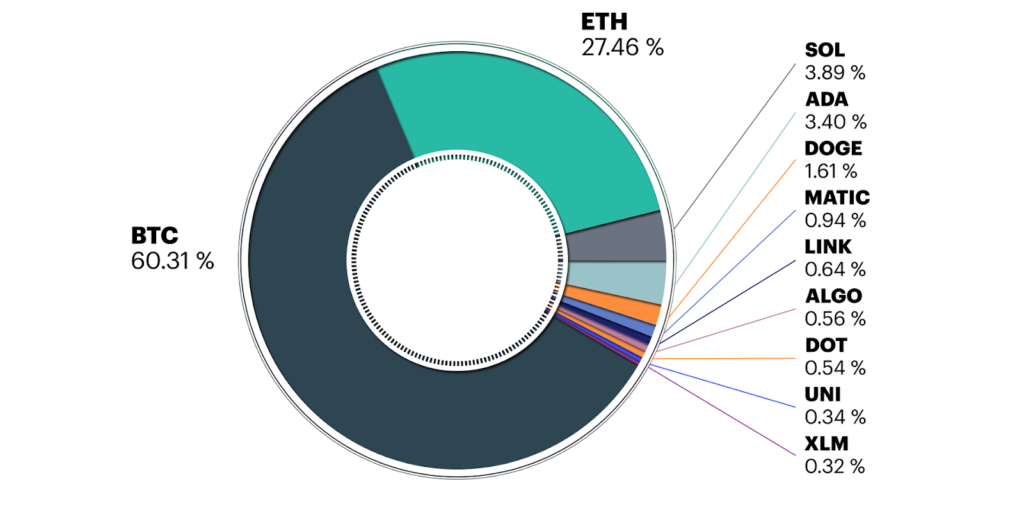

Market capitalization:

Source: CF Benchmarks, as of March 1, 2022

By applying a fixed cap of 25% to these weights, bitcoin and ether would exceed the cap at inception, with no difference in weighting based on market capitalization or liquidity. Different capping weights would result in similar results and lead to the index trading more like a fixed weight index than a market capitalization weighted index.

The point on liquidity is probably the most impactful for a small burgeoning asset category like cryptocurrency. For an index to be representative of the market it needs to be tradable. Smaller constituents generally have a significantly lower liquidity profile, thus making it difficult for institutional managers to replicate the market beta when the smaller constituents receive a higher weighting that results from capping the very largest constituents. Therefore an index that significantly re-weights to much smaller and illiquid names creates a benchmark that may not be representative or tradable.

So how to solve this problem? Instead of applying a fixed cap, the index will benefit from a smoothed capitalization methodology where each additional percentage weight is discounted sequentially more than the previous one by a defined amount. This progressive redistribution from large to small caps benefits from keeping the final index weights relatively close to free float market capitalization while still achieving diversification.

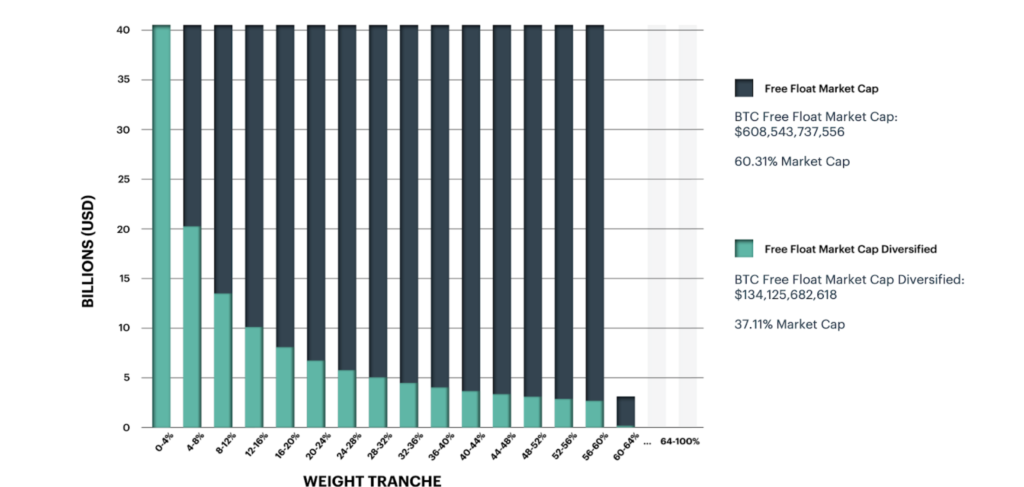

In order to achieve the smooth capitalization redistribution, the discounting will increase exponentially using the inverse step function applied to each additional 4% bucket. The inverse stepped function basically reduces each tranche by 1/ nth tranche. To illustrate, if we were to apply the inverse step function with a 4% tranche to the 60.31% market capitalization weight to bitcoin, you would have a process that looks like the following chart and we have a new bitcoin index weight of 37.11%.

Bitcoin diversification step example:

Source: CF Benchmarks, as of March 1, 2022

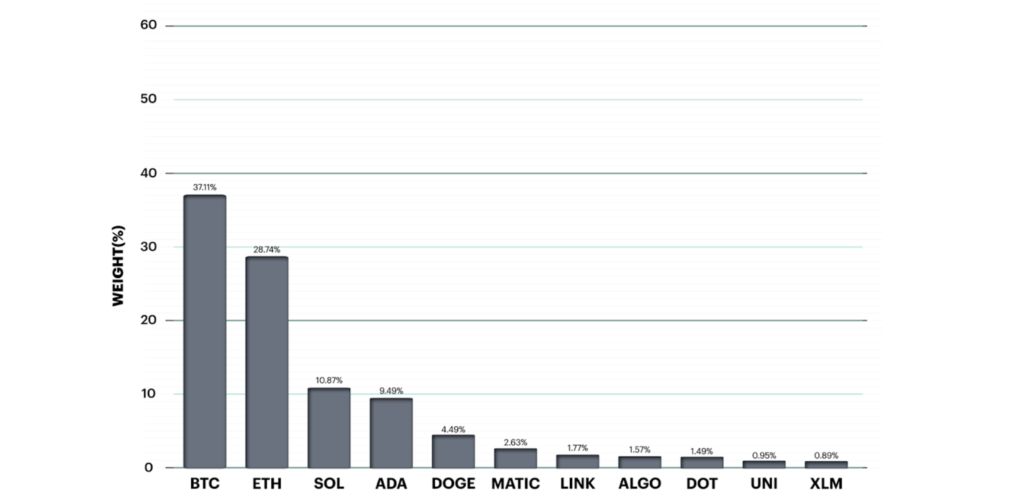

By applying this process to the whole index you achieve a redistribution that looks like the following.

Diversified weights:

Source: CF Benchmarks, as of March 1, 2022

The smoothed capitalization redistribution allows investors to achieve the primary goals of a market capitalization weighted index, to be representative of the market, to reduce concentration to the largest weights and to remain tradeable.

Our blog series continues tomorrow with a discussion on how the use of index inclusion and exclusion screens can be used to help reduce risk.

The products and services offered by Arxnovum are available to qualified investors in certain provinces and territories of Canada. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All investments contain risk and may lose value. Investing in the cryptocurrency market is subject to risks. Cryptocurrency, often referred to as “virtual currency” or “digital currency”, operates as a decentralized, peer-to-peer financial exchange and value storage that is used like money. Cryptocurrency operates without the oversight of a central authority or the banks and is not backed by any government. Even indirectly, cryptocurrencies such as bitcoin may experience high volatility, and related investment vehicles may be affected by such volatility. Cryptocurrency is not legal tender. Federal, state, provincial, territorial or foreign governments may restrict the use and exchange of cryptocurrency, and regulation in North America is still developing. Cryptocurrency trading platforms may stop operating or permanently shut down due to fraud, technical glitches, hackers or malware, which could have an adverse impact on the net asset value per unit of the Fund. Please consult the Funds Term Sheet for a complete list of risks. Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Arxnovum Investments Inc. and the portfolio manager believe to be reasonable assumptions, neither Arxnovum Investments Inc. nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.