Across financial assets there are new dynamics on prices and yields as the US Federal Reserve (the Fed) has moved from passively watching inflationary pressures building to economic prints of 8.3% annual inflation. Against this backdrop there is a war in the Ukraine and Covid lockdowns in major Chinese cities. In our opinion, the main force impacting all risky assets is the Fed’s race to deal with inflation and we see them as woefully behind the curve.

US CPI year-over-year

In order to address the rising inflation levels that have clearly moved well past transitory, the Fed has embarked on an aggressive path of increasing interest rates. Having already increased the influential fed funds rate by 75 bps (100 bps = 1.00%) at its last two meetings, the Fed has signalled to the market to expect more increases at future meetings.

As US rates rise, capital will flow into the US and strengthen the US dollar (USD). This has been evident in the Yen and the Euro. Our view is that the USD is the largest asset globally. Its recent strength means that anything priced in USD is falling – from bond prices to equities to commodities to bitcoin and cryptocurrencies.

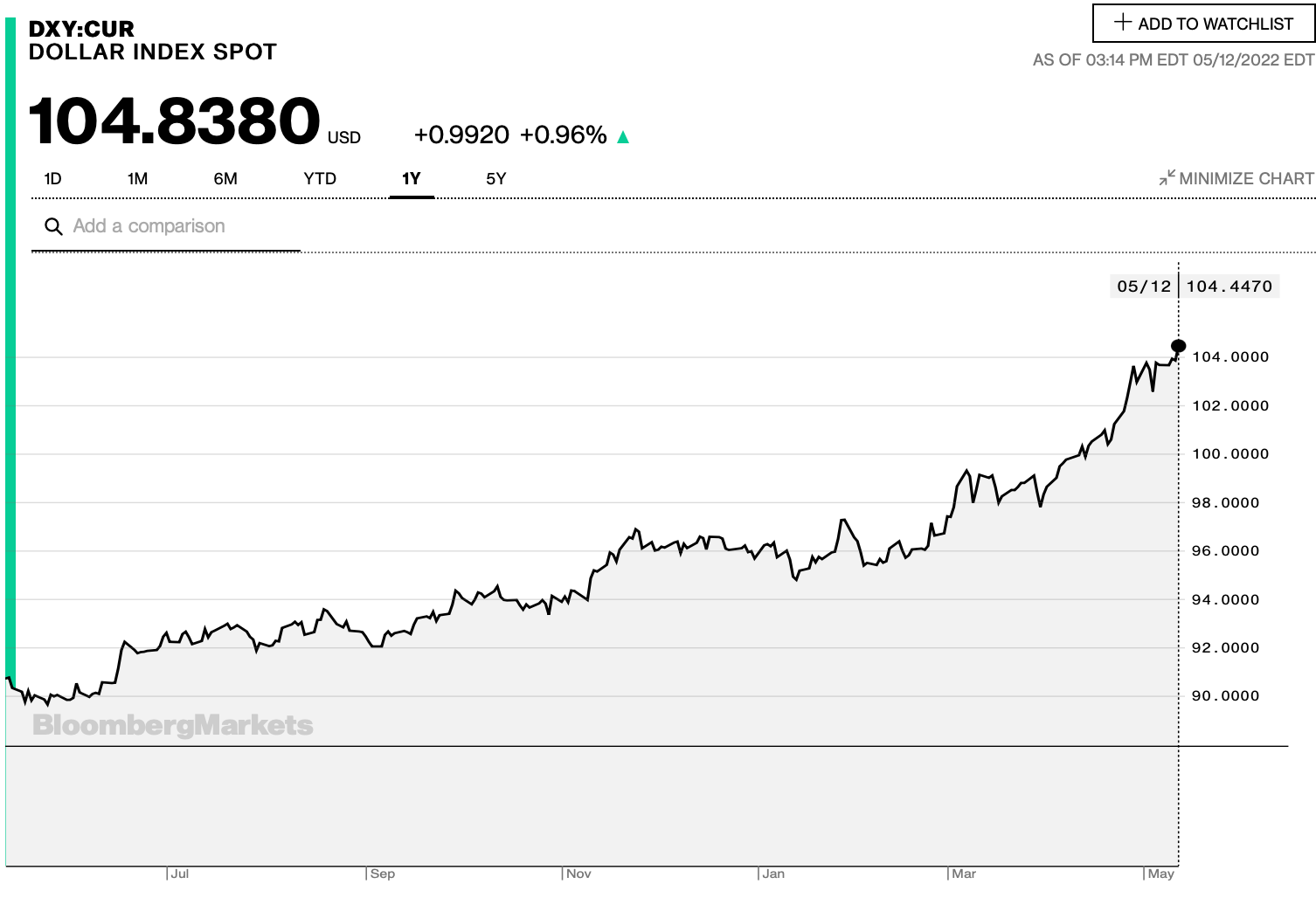

The strengthening US dollar can be witnessed through the US Dollar Index (Ticker: DXY), which is an index that measures the value of the US dollar relative to a basket of foreign currencies, including Euro, Japanese yen, British pound, Canadian dollar, Swedish krona and Swiss franc. The 15% move higher in the US Dollar Index over the last year has been driven by expectations for higher rates and by a flight to safety in the face of geopolitical tensions around the globe.

Source: Bloomberg.com

The US dollar should revert to a weakening trend if rates return to a path lower to the zero-interest-rate boundary and this will occur if there is a U.S. recession or severe market crash or both. The US yield curve has inverted which is seen as an advanced signal of a recession. The next signal to watch is the unemployment rate against its 12 month moving average.

The digital asset market has not escaped the drawdown we’ve seen in other risky assets. The CF Diversified Large Cap Crypto Index which measures a basket of the largest and most liquid crypto currencies is down 49% year to date. Bitcoin which is the largest, oldest and widely seen as one of the safer crypto currencies has not avoided the market carnage with the CME CF Bitcoin Reference Rate Index down 36% year to date.

Crypto currency markets were further roiled this past week with an algorithmic stablecoin called Terra depegging from the USD$1 it was meant to maintain. From what we have seen this was an engineered attack, but no matter, our funds have no direct exposure to Terra, Luna nor Anchor. Part of the Terra/Luna defence was to have bitcoin reserves which may have been sold in haste causing the fall in bitcoin prices. Bitcoin is in a time period relative to its past halving where the price tends to move sideways as we move towards the next halving, which will be in May 2024. We are watching the markets closely and welcome questions from our investors.

Disclosures

The products and services offered by Arxnovum are available to qualified investors in certain provinces and territories of Canada. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All investments contain risk and may lose value. Investing in the cryptocurrency market is subject to risks. Cryptocurrency, often referred to as “virtual currency” or “digital currency”, operates as a decentralized, peer-to-peer financial exchange and value storage that is used like money. Cryptocurrency operates without the oversight of a central authority or the banks and is not backed by any government. Even indirectly, cryptocurrencies such as bitcoin may experience high volatility, and related investment vehicles may be affected by such volatility. Cryptocurrency is not legal tender. Federal, state, provincial, territorial or foreign governments may restrict the use and exchange of cryptocurrency, and regulation in North America is still developing. Cryptocurrency trading platforms may stop operating or permanently shut down due to fraud, technical glitches, hackers or malware, which could have an adverse impact on the net asset value per unit of the Fund. Please consult the Funds Term Sheet for a complete list of risks. Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Arxnovum Investments Inc. and the portfolio manager believe to be reasonable assumptions, neither Arxnovum Investments Inc. nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.